Ridge Regression

Before introducing Ridge Regression, let’s have a brief look at Linear Regression. Linear Regression is one of the simplest yet fundamental statistical learning techniques. It is a great initial step towards more advanced and computationally demanding methods.

Linear regression examines the relationship between a dependent variable and one or more independent variables. Linear regression with p independent variables focuses on fitting a straight line in p+1-dimensions that passes as close as possible to the data points in order to reduce error.

General Characteristics of Linear Regression:

- A supervised learning technique

- Useful for predicting a quantitative response

- Attempts to fit a function to predict a response variable

- The problem is reduced to a parametric problem of finding a set of parameters

- The function shape is limited (as a function of the parameters)

The idea behind Linear Regression is that we reduce the problem of estimating the response variable, Y, by assuming there is a linear function of the predictor variables, X1, X2,… which describes Y. This reduces the problem to that of solving for the parameters β0, β1, β2, …, βn in the equation:

With a single predictor, we are expected to fit a function to the data similar to the following:

But allowing predictors of higher orders, it is possible to fit a non-linear function of the original predictors:

The above equation for the assumption of the shape of the function is called the hypothesis function and this can be written in matrix notation as (θ is used here instead of β)

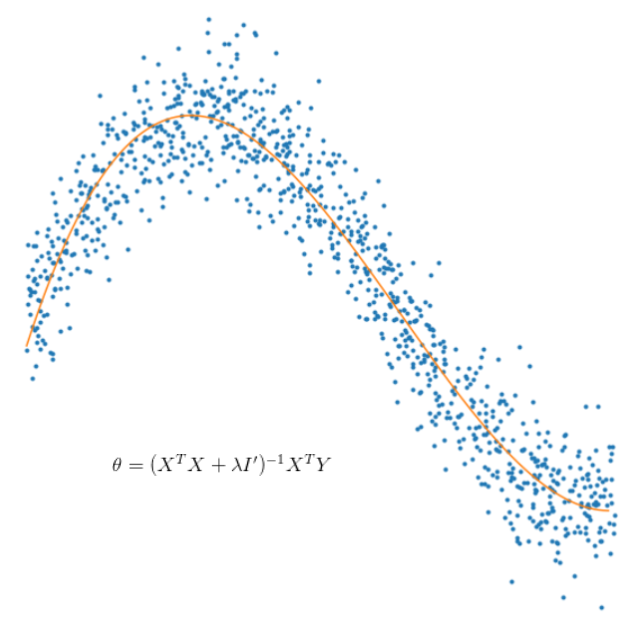

We are looking to find a vector θ which minimises the errors between the values given by the hypothesis function (the orange line in the graphs above) and the actual response variables on known data. Mathematically, the equation we need to minimise is

.

.  is the error resulting from the

is the error resulting from the  prediction and the actual value,

prediction and the actual value,  .

. Now we can find the derivative of the Cost function thanks to the index representation since all terms are scalar

Setting this to zero and solving

The extra step we will be taking here to introduce Ridge Regression is to add an additional term in this equation which is the L2-norm

where

Differentiating, and setting to zero, the solution then is slightly different from that for Linear Regression

where

L = 0.2

normalize = False

# Convert the predictor dataframe and the response dataframe to arrays to be consistent with data type

X = np.concatenate((np.ones((X.shape[0],1)),np.array(X)),axis=1)

y = np.array(y)

ncols = X.shape[1]

if normalize:

# standardise X if required - Can be vectorised using broadcasting

for i in range(1,ncols):

X[:,i] = (X[:,i] - np.mean(X[:,i]))/np.std(X[:,i])

# standardise y if required

y = (y - np.mean(y))/np.std(y)

# Create transpose (3 X n)

X_T = X.transpose()

# Calculate X^T X (3 X 3)

XTX = X_T.dot(X)

# Create I'

Id = np.eye(XTX.shape[0])

Id[0,0] = 0

# Add the shrinkage factor part

XTX = XTX + L*Id

# calculate inverse of XTX + lambda I' (3 X 3)

XTX_inv = np.linalg.inv(XTX)

# Calculate theta

theta = XTX_inv.dot(X_T.dot(y))

Now that we have the calculation for θ, we can look at the p-values corresponding to the θ‘s

Let

![E[\hat{\theta}]=\theta](https://s0.wp.com/latex.php?latex=E%5B%5Chat%7B%5Ctheta%7D%5D%3D%5Ctheta&bg=ffffff&fg=000&s=0&c=20201002)

![E[ \hat{Y} ]=Y](https://s0.wp.com/latex.php?latex=E%5B+%5Chat%7BY%7D+%5D%3DY&bg=ffffff&fg=000&s=0&c=20201002)

are the residuals

are the residualsand

In Python code (where ridgeModel is our fitted statsmodels.api Ridge Regression model)

# Get the coefficient solutions from the model

coefs = np.append(ridgeModel.params[0],ridgeModel.params[1:])

# Get the predictions (X_new includes the constant term)

predictions = ridgeModel.predict(X_new)

# Calculate the MSE

MSE = (sum((y-predictions)**2))/(len(X_new)-len(X_new.columns))

# Calculate the variance

var = MSE*(np.linalg.inv(np.dot(X_new.T,X_new)).diagonal())

# Calculate the standard deviation

sd = np.sqrt(var)

# Calculate the t-statistics

t = coefs/ sd

# Calculate the p-values using the t-statistics and the t-distribution (2 is two-sided)

p_values =[2*(1-stats.t.cdf(np.abs(i),(len(X_new)-1))) for i in t]

# 3 decimal places to match statsmodels output

var = np.round(var,3)

t = np.round(t,3)

p_values = np.round(p_values,3)

# 4 decimal places to match statsmodels

coefs = np.round(coefs,4)

summary_df = pd.DataFrame()

summary_df["Features"],summary_df["coef"],summary_df["std err"],summary_df["t"],summary_df["P > |t|"] = [

X_new.columns,coefs,sd,t,p_values]

print(summary_df)

We can extend the Ridge class of SKLearn to give it the ability to calculate p-values (full class at the end of this article). This module can either be found here or simply install the package from PyPi as follows

pip install model_arena

Then import and use it as follows on a housing dataset as an example (found here )

# The module containing our custom RidgeRegression class

from model_arena import RidgeRegression

# Predictor variables

X = housePrice.drop('SalePrice',axis=1)

# Response variable

y = housePrice['SalePrice']

# Create a RidgeRegression object

rm = RidgeRegression()

# Run the feature selection method as above to limit to the most important variables.

# Stores the order of variables to the object

rm.featureSelection(X,y)

# Find the value of alpha minimising MSE for these features

rm.findBestAlpha(X[rm.bestMeanCVModel],y)

# Print the alpha

print('Alpha = {}'.format(rm.alpha))

# Fit the model with the best features and the alpha

rm.fit(X[rm.bestMeanCVModel],y)

# Display a summary including p-values

rm.summary(X[rm.bestMeanCVModel],y)

This will produce an output similar to the following (note that ‘MSE’ and ‘Negative MSE’ are used interchangeably here. SKLearn uses ‘Negative MSE’)

The output is designed to look similar to statsmodels.api and setting the shrinkage factor alpha=0 should recover the statsmodels.api output for Linear Regression (note the shrinkage factor lambda is called alpha in SKLearn’s Ridge class)

Running Ridge Regression with alpha = 0 and then with an optimised alpha as above, it can be seen that it is possible to improve on Linear Regression MSE as well as reduce the variance of the predictions from the model. In code

# Compare summary outputs between Ridge Regression and Linear Regression

print('RIDGE REGRESSION SUMMARY')

rm.summary(X_train,y_train)

print('\n\nLINEAR REGRESSION SUMMARY')

rmlm = RidgeRegression(alpha=0)

rmlm.fit(X_train,y_train)

print('Parameters of the linear regression model = {}'.format([rmlm.intercept_,rmlm.coef_]))

rmlm.summary(X_train,y_train)

# Predict a new set of points and find MSE for Linear Regression and Ridge Regression

print('Linear Regression MSE = {}'.format((rmlm.predict(X_test) - y_test).dot(rmlm.predict(X_test) - y_test)))

print('Ridge Regression MSE = {}'.format((rm.predict(X_test) - y_test).dot(rm.predict(X_test) - y_test)))

# Confirm that the standard deviation of predictions is smaller for Ridge Regression than for Linear Regression

rmpredictions = []

for i,j in list(zip(list(X_test.values),list(y_test))):

rmpredictions.append(rm.predict(i.reshape(1,-1)))

rmlmpredictions = []

for i,j in list(zip(list(X_test.values),list(y_test))):

rmlmpredictions.append(rmlm.predict(i.reshape(1,-1)))

print('Standard deviation of Linear Regression predictions = {}'.format(np.std(rmlmpredictions)))

print('Standard deviation of Ridge Regression predictions = {}'.format(np.std(rmpredictions)))

A more in-depth investigation can be found here and an application of Linear/Lasso/Ridge regression on Kaggle’s housing dataset can be found here.

Summary

We have seen the following:

- Ridge Regression is an extension of Linear Regression by constraining the coefficients in the Cost function.

- Ridge regression reduces the variance of the predictions it provides

- Setting the shrinkage factor to zero in Ridge Regression means the Cost function is identical to that of Linear Regression and thus the results are identical too

- It is possible to extend SKLearn’s Ridge class (example given at the end of this article) to also calculate p-values for Ridge Regression

Supplementary Material

class RidgeRegression(Ridge):

'''

This class inherits from the Ridge class in the sklearn package. It extends that class by

adding the capability to produce p-values, run feature selection and find the best alpha

which minimises the MSE

'''

def summary(self,X,y):

'''

This method produces a summary similar to the one produced by statsmodels.api.

It includes the coefficients and their p-values in a summary table

:param X: features array

:param y: response array

'''

# This will store the coefficients of the model that has already been run

coefs = []

# If the model was fit with an intercept

if 'intercept_' in dir(self):

coefs = np.append(self.intercept_,self.coef_)

else:

coefs = self.coef_

# Get the predictions

predictions = self.predict(X)

# If a constant column needs to be added (determine this dynamically)

if len(X.columns) < len(coefs):

X = X.copy()

X.insert(0,'Const',1)

# Calculate the MSE

MSE = (sum((y-predictions)**2))/(len(X)-len(X.columns))

# Calculate the variance

var = MSE*(np.linalg.inv(np.dot(X.T,X)).diagonal())

# Calculate the standard deviation

sd = np.sqrt(var)

# Calculate the t-statistics

t = coefs/ sd

# Calculate the p-values using the t-statistics and the t-distribution (2 is two-sided)

p_values =[2*(1-stats.t.cdf(np.abs(i),(len(X)-1))) for i in t]

# 3 decimal places to match statsmodels output

var = np.round(var,3)

t = np.round(t,3)

p_values = np.round(p_values,3)

# 4 decimal places to match statsmodels

coefs = np.round(coefs,4)

# Summary dataframe

summary_df = pd.DataFrame()

summary_df["Features"],summary_df["coef"],summary_df["std err"],summary_df["t"],summary_df["P > |t|"] = [X.columns,

coefs,sd,t,p_values]

print(summary_df)

def findBestAlpha(self,X,y,silent=True):

'''

This method keeps changing alpha until the MSE is reduced as much as it can be reduced. This

alpha selection depends on input datasets

:param X: features array

:param y: response array

:param silent: if True, then progress is omitted

'''

silent = True

alpha = 1

prevAlpha = None

bestMSE = None

tol = 0.000001

doublingMode = True

# Here, we start by continuously doubling alpha until we get to a point where the MSE doesn't increase

# Then, at this point, we switch to incrementing (or decrementing) by smaller amounts until the tolerance is reached

while True:

# Calculate the MSE using this alpha

thisMSE = np.mean(cross_val_score(RidgeRegression(alpha=alpha),X,y,scoring='neg_mean_squared_error',cv=10))

if not silent:

print('alpha = {}\nbestMSE = {}\nthisMSE = {}\n#############'.format(alpha,bestMSE,thisMSE))

# if doubling mode

if doublingMode:

# update bestMSE

if (not bestMSE) or (bestMSE < thisMSE):

bestMSE = thisMSE

else:

if not silent:

print('Doubling Finished!!!!')

# switch the mode and roll back alpha to the previous one

doublingMode = False

tempAlpha = prevAlpha

prevAlpha = alpha

alpha = tempAlpha

continue

# update alpha

prevAlpha = alpha

alpha = (alpha + 0.001)*2

else:

# update alpha to |alpha-prevAlpha|/2 away from where it currently is (in either direction)

ghostPoint = alpha + (alpha - prevAlpha)

nextAlpha1 = (prevAlpha + alpha)/2

nextAlpha2 = (alpha + ghostPoint)/2

# The Ridge class has numerical issues when alpha is close to zero

if(nextAlpha1 < 0.0001):

nextAlpha1 = 0.0001

if(nextAlpha2 < 0.0001):

nextAlpha2 = 0.0001

# Calculate the MSE on either side of alpha

MSE1 = np.mean(cross_val_score(RidgeRegression(alpha=nextAlpha1),X,y,scoring='neg_mean_squared_error',cv=10))

MSE2 = np.mean(cross_val_score(RidgeRegression(alpha=nextAlpha2),X,y,scoring='neg_mean_squared_error',cv=10))

# Choose to MSE and the corresponding alpha of the one that is better

if (MSE1 > MSE2) and (MSE1 > bestMSE) and (np.abs(prevAlpha - alpha) > tol):

prevAlpha = alpha

alpha = nextAlpha1

bestMSE = MSE1

elif (MSE2 > MSE1) and (MSE2 > bestMSE) and (np.abs(prevAlpha - alpha) > tol):

prevAlpha = alpha

alpha = nextAlpha2

bestMSE = MSE2

else:

if (np.abs(prevAlpha - alpha) > tol):

# pull prevAlpha closer to alpha

prevAlpha = (prevAlpha + alpha)/2

else:

alpha = prevAlpha

break

self.alpha = alpha

print('Ridge Regression MSE = {}, best alpha = {}'.format(bestMSE,alpha))

def featureSelection(self,X,y):

'''

This method iterates and adds a new feature to the features list in the

order of best improvement of MSE

:param X: features array

:param y: response array

'''

# Run through each model in the correct order and run CV on it and save the best CV score

bestMeanCV = -1

bestMeanCVModel = []

oldArraySize = 0

columnsArray = X.columns.copy()

while oldArraySize != len(X):

bestPredictor = ''

oldArraySize = len(X.columns)

for i in columnsArray:

thisModel = bestMeanCVModel.copy()

thisModel.append(i)

# First set X to be the full set of remaining parameters

x = X.loc[:,thisModel]

if len(x.columns) == 1:

linregCVScores = cross_val_score(Ridge(alpha=6),x.values.reshape(-1,1),y,scoring='neg_mean_squared_error',cv=10)

else:

linregCVScores = cross_val_score(Ridge(alpha=6),x,y,scoring='neg_mean_squared_error',cv=10)

if bestMeanCV > -linregCVScores.mean():

bestMeanCV = -linregCVScores.mean()

bestPredictor = i

elif bestMeanCV == -1:

bestMeanCV = -linregCVScores.mean()

bestPredictor = i

if bestPredictor not in columnsArray:

break

columnsArray = columnsArray.drop(bestPredictor)

bestMeanCVModel.append(bestPredictor)

print('{} was added with test MSE {}'.format(bestMeanCVModel[-1],bestMeanCV))

self.bestMeanCVModel = bestMeanCVModel

self.bestMeanCV = bestMeanCV

print('The final best model is {} and its TEST MSE is {}'.format(bestMeanCVModel,bestMeanCV))